Russia's 2025 GDP Revealed: $1.09 Trillion

Russia’s wartime economy has become increasingly difficult to measure through headline statistics alone. Large-scale state spending, sanctions distortions, military-industrial prioritisation, exchange-rate volatility and changing reporting standards have all reduced the transparency of traditional macroeconomic indicators. As a result, alternative analytical frameworks are often used to understand the underlying structure of output.

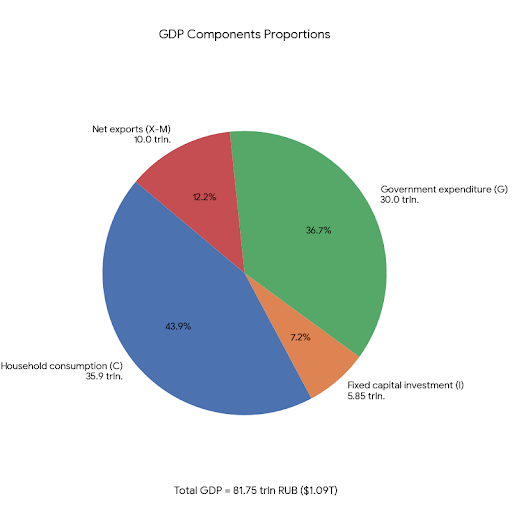

Household Consumption Remains the Largest Economic Base

The result suggests that domestic demand remains the primary source of economic activity. Even in a wartime environment, Russia’s economy still depends heavily on everyday spending by households rather than on exports alone.

However, the quality of consumption matters. If incomes are pressured by inflation, layoffs or wage arrears, then nominal consumption may remain positive while real purchasing power weakens.

From a structural perspective, this means the economy still stands on internal demand — but that demand may be increasingly fragile.

The consumption side of the economy appears increasingly uneven. While defence-linked sectors may remain active, multiple domestic indicators point to stress in civilian employment and private demand.

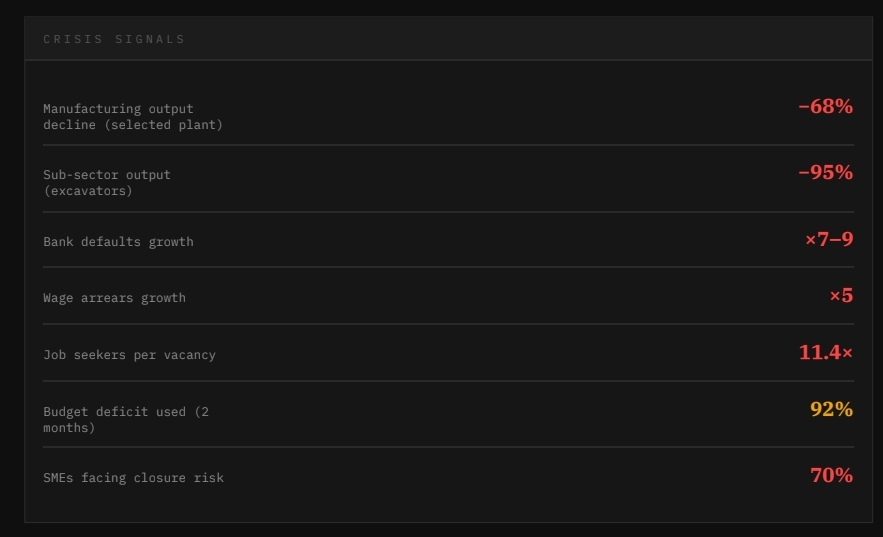

Russia’s HeadHunter labour index reportedly reached 11.4 applicants per vacancy in March 2026, compared with 4.8 one year earlier. In St. Petersburg, the figure exceeded 12, which some local analysts described as crisis territory.

Investment Weakness Appears to Be the Core Constraint

This pattern shows that high interest rates, sanctions-related equipment shortages, weak demand and rising costs are discouraging long-term expansion. In practical terms, Russia may still be producing, but it is investing less into future productive capacity.

A survey referenced in Russian sources found 70% of small and medium businesses see risk of closure or bankruptcy in the near term.

Industrial examples reinforce the trend. At Cherepovets Foundry, reported output fell sharply year-on-year, while some sectors such as industrial machinery saw collapses in selected product lines. Russian sources also cite a 7–9x increase in enterprises in de facto bank default, suggesting firms are struggling to refinance working capital.

Technically, this is one of the most serious macro signals: when companies stop investing, future productivity and growth potential decline even if current GDP remains supported.

The car market is the mirror of the economy. In 2012, Russia sold 2.9 million cars. In 2025, it sold 1.3 million — down more than 50% from the peak. The fleet itself shrank for the first time since 2000." — Roman Romanov, analyst.

Government deficit today, for future generations liability.

The strongest pillar in the model is government expenditure, estimated at 30 trillion RUB. This is consistent with wartime economics, where public spending offsets weakness in investment and private demand.

However, domestic fiscal signals indicate growing strain. Russia’s federal deficit reached 3.5 trillion RUB in January–February 2026, equal to 92% of the annual planned deficit target.

Additional pressure is visible at the regional level. Russian reports cite wage reductions and delayed payments in healthcare systems across multiple regions:

Kurgan nurses lost bonus payments

Vladimir ambulance workers received symbolic January bonuses

Tuva medical staff reportedly received only partial advances.

$1.09 trillion is not a round number chosen for effect. It is the output of a standard national accounts model applied to components that are each individually consistent with the ground-level data emerging from Russia's own industrial sector, financial system and labour market. The model number and the real-world signals point in the same direction. The question is not whether the decline is real. The question is how much further it goes.